Let's talk about the Australian housing slowdown and what house prices in Australia are likely to do over the next two years.

Last year saw national average house prices rise by 22%, the fastest 1-year increase since 1989. Propelled by low-interest rates, low stock and high demand post covid lockdowns, national house prices are expected to peak around mid-2022. Due to a combination of other factors likely to fall by 10% to 15% between then and 2024.

I frequently hear people say house prices never fall, but it’s simply not true. Sydney house prices have fallen many times over the years - 41% between 1937 and 1941, then, 14% in 1947-48, 12% in 1951-53, 22% in 1961-62, 22% in 1974-77, 10% in 1980-83, 8% in 1989-91, 7% in 2008-09, and then in 2022-24? Time will tell.

Of course, over the longer-term property prices always go up, just like the share market, but sadly most young families today have never experienced this before as we have had such a stellar run.

The main reason why it’s likely to fall?

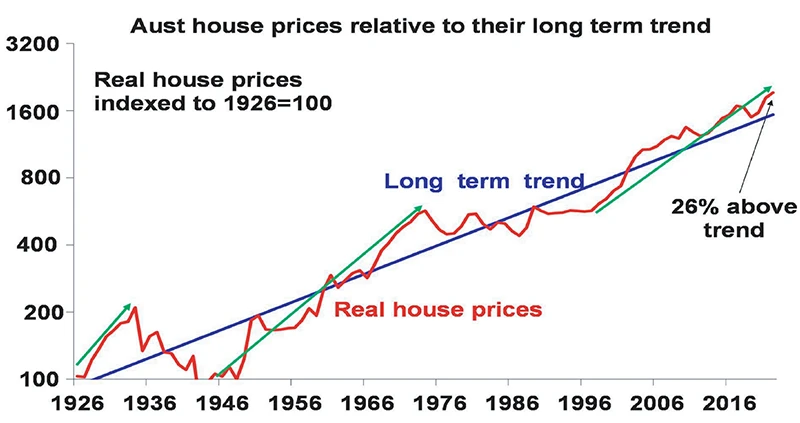

- Poor affordability as property has risen 358% over the past 25 years compared to a 113% rise in wages.

- Increase in interest rates coming off a 50-year low.

- Higher inflation.

- Increase in sellers and supply.

- The decline in homebuyer confidence.

Don’t PANIC is the key and ensure you can ride out an interest rate hike of at least 2% in the medium term. It’s unlikely we’ll see a full-blown property crash as world governments will be slow to increase interest rates as this is a global issue. Vacancy rates remain low, and most households are well-positioned to manage higher interest rates.

So, are we nearing the end of a 25-year housing boom?

Over the past 100 years, we have seen major long-term housing booms in Australia. These periods were the late 1920s, post-WW2 and the mid-1990s - all predominantly driven by low-interest rates and high demand.

Source: ABS, AMP

So, the conclusion is to expect a fall in house prices and to be prepared. The best way to be prepared is to know your financial position on cash flow, budget and mortgage.

Most people do not have a debt strategy that ensures they can be debt-free before retiring, and that’s where we can make sure you don’t fall into that trap.

Not sure how to prepare and make sure you can ride out the next two years?

Speak with one of our Financial Planners about the best approach for your circumstances, either book a meeting or get in contact with us on 02 9328 0876.

Article by Bill Bracey | Principal &| Senior Financial Planner

General Disclaimer: This article contains information that is general in nature. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decisions based on this information. Please seek personal financial advice prior to acting on this information.