...but there’s a few storm clouds around.

Key points

- 2017-18 saw strong returns for diversified investors, but it was a story of two halves with strong December half returns but more volatility in the past 6 months.

- Key lessons for investors from the last financial year include: turn down the noise around financial markets, maintain a well-diversified portfolio; be cautious of the crowd; and cash continues to provide low returns.

- Returns are likely to slow and the volatility of the last six months is likely to continue. Global growth is good, this should underpin profit growth and there are minimal signs of economic excess that point to a peak in the global growth cycle. But rising US inflation and rates, Trump and trade war fears and the risks around China and emerging countries are the main threats.

Introduction

The past financial year saw solid returns for investors but it was a story of two halves. While the December half year was strong as global share markets moved to factor in stronger global growth and profits helped by US tax cuts, the last six months have been messier and more constrained – with US inflation and interest rate worries, trade war fears, uncertainty around Italy, renewed China and emerging market worries and falling home prices in Australia. But will returns remain reasonable or is the volatility of the past six months a sign of things to come? After reviewing the returns of the last financial year, this note looks at the investment outlook for 2018-19 financial year.

A good year for diversified investors

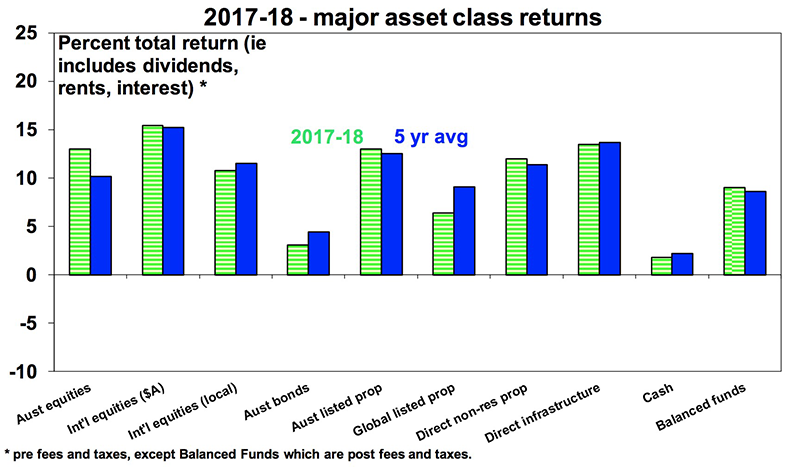

The 2017-18 financial year saw yet again pretty solid returns for well diversified investors. Cash and bank deposits continued to provide poor returns and the combination of low yields and a back-up in some bond yields saw low returns from bonds. The latter resulted in mixed returns from yield sensitive investments, but Australian real estate investment trusts performed well helped by the RBA leaving rates on hold.

Reflecting strong gains in the December half as investors moved to factor in stronger global growth and profits assisted in the US by tax cuts global shares returned 11% in local currency terms and 15% in Australian dollar terms. Australian shares also performed well with the ASX 200 rising to a 10-year high and solid dividends resulting in a total return of 13%. Unlisted assets have continued to benefit from “search for yield” investor demand and faster growth in “rents” with unlisted property returning around 12% and unlisted infrastructure returning around 13.5%.

As a result, balanced growth superannuation returns are estimated to have returned around 9% after taxes and fees which is pretty good given inflation of 2%. For the last five years balanced growth super returns have also been around 8.5% pa.

Source: Thomson Reuters, AMP Capital

Australian residential property slowed with average capital city prices down 1.6%, with prices down in Sydney, Perth and Darwin. Average returns after costs were around zero.

Key lessons for investors from the last financial year

These include:

- Be cautious of the crowd – Bitcoin provided a classic reminder of this with its price peaking at $US19500 just when everyone was getting interested in December only to then plunge 70% in price.

- Turn down the noise – despite numerous predictions of disaster it turned out okay.

- Maintain a well-diversified portfolio – while cash, bonds and some yield sensitive listed assets had a tougher time, a well-diversified portfolio performed well.

- Cash is still not king – while cash and bank deposits provided safe steady returns, they remain very low.

Expect more constrained returns and volatility

We expect returns to slow a bit over the new financial year and just as we have seen over the last six months volatility is likely to remain high. First the positives:

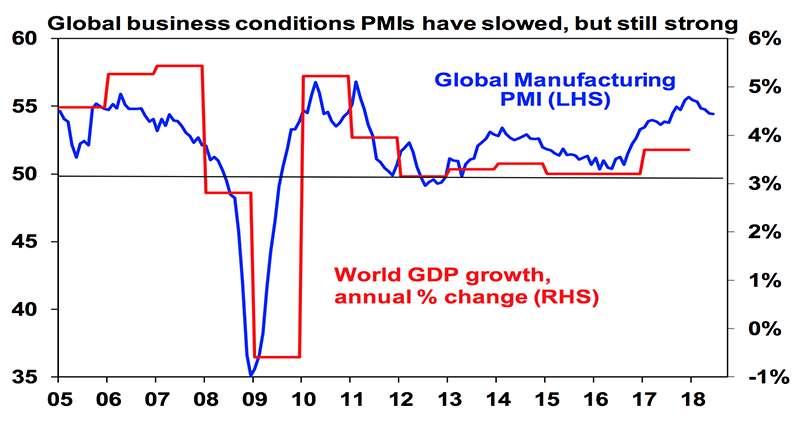

- While global growth looks to have passed its peak the growth outlook remains solid. Business conditions indicators – such as surveys of purchasing managers (Purchasing Managers Indexes or PMIs) – are off their highs and point to some moderation in growth, but they remain strong pointing to solid global overall.

Source: Bloomberg, AMP Capital

In Australia, growth is likely to remain between 2.5% and 3% with strong business investment and infrastructure helping but being offset by a housing slowdown and constrained consumer spending.

- Second, solid economic growth should continue to underpin solid profit growth from around 7% in Australia to above 10% globally

- Third, while we are now further through the global economic cycle there is still little sign of the sort of excess that normally brings on an economic downturn – there is still spare capacity globally, growth in private debt remains moderate, investment as a share of GDP is around average or below, wages growth and inflation remain low and we are yet to see a generalised euphoria in asset prices.

- Fourth, global monetary policy remains very easy with the Fed continuing to raise rates gradually, the ECB a long way from raising rates and tightening in Japan years away.

- Finally, share valuations are not excessive. While price to earnings ratios are a bit above long-term averages, this is not unusual for a low inflation environment. Valuation measures that allow for low interest rates and bond yields show shares to no longer be as cheap as a year ago but they are still not expensive, particularly outside of the US.

Against this though there are a few storm clouds:

- First, the US economy is more at risk of overheating – unemployment is at its lowest since 1969, wages growth is gradually rising and inflationary pressures appear to be picking up. The Fed is aware of this and will continue its process of raising rates. While other countries are behind the US, its share market invariably sets the direction for global markets

- Second, global liquidity conditions have tightened compared to a year ago with central bank quantitative easing slowing down and yield curves (ie the gap between long term and short-term bond yields) flattening.

- Third, the risks of a trade war dragging on global growth have intensified. While the share of US imports subject to recently imposed tariffs is minor so far (at around 3%) they are threatened to increase. Our base case remains that some sort of negotiated solution will be reached but trade war worries could get worse before they get better.

- Fourth, emerging countries face various risks from several problem countries (Turkey, Brazil and South Africa), slowing growth in China, concerns the rising US dollar will make it harder for emerging countries to service their foreign debts and worries they will be adversely affected by a trade war.

- Finally, various geopolitical risks remain notably around the Mueller inquiry in the US, the US mid-term elections and Italy heading towards conflict with the EU over fiscal policy.

A problem is that various threats around trade and Trump, Italy and China have come along at a time when the hurdle for central banks to respond may be higher than in the past – with the Fed focussed on inflation and the ECB moving to slow its stimulus and less inclined to support Italy.

What about the return outlook?

Given these conflicting forces it is reasonable to expect some slowing in returns after the very strong returns seen in the last two years. Solid growth, still easy money and okay valuations should keep returns positive, but they are likely to be constrained and more volatile thanks to the drip feed of Fed rate hikes, trade war fears, China and Emerging Market worries and various geopolitical risks. In Australia, falling home prices in Sydney and Melbourne along with tightening bank lending standards will be drags. Looking at the major asset classes:

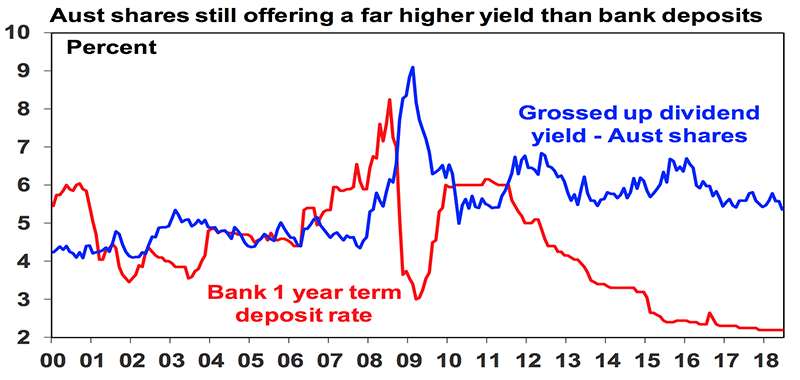

- Cash and bank deposit returns are likely to remain poor at around 2% as the RBA is expected to remain on hold out to 2020 at least. Investors still need to think about what they really want: if it’s capital stability then stick with cash but if it’s a decent stable income then consider the alternatives with Australian shares and real assets such as unlisted commercial property continuing to offer attractive yields.

Source: RBA; AMP Capital

- Still ultra-low sovereign bond yields and the risk of a risking trend in yields, which will result in capital losses, are likely to result in another year of soft returns from bonds.

- Unlisted commercial property and infrastructure are likely to benefit from the ongoing “search for yield” (although this is waning) and okay economic growth.

- Residential property returns are likely to be mixed with Sydney and Melbourne prices falling, Perth and Darwin bottoming and other cities providing modest gains.

- Shares are at risk of a further correction into the seasonally weak September/October period given the storm clouds noted above, but okay valuations, reasonable economic growth and profits and still easy monetary conditions should see the broad trend in shares remain up – just more slowly. We continue to favour global shares over Australian shares.

- Finally, the $A is likely to fall as the RBA holds and the Fed hikes adding to the case for unhedged global shares.

Things to keep an eye on

The key things to keep an eye are: global business conditions PMIs for any deeper slowing; risks around a trade war; risks around Trump ahead of the US mid-term elections; the drip feed of Fed rate hikes; conflict with Italy over fiscal policy in Europe; risks around China and emerging countries; and the Australian property market – where a sharp slump in home prices (which is not our view) could threaten Australian growth.

Concluding comments

Returns are likely to remain okay over 2018-19 as conditions are not in place for a US/global recession. But expect more constrained returns (say around 6% for a diversified fund) and continued volatility.

Still have some questions?

If you want to discuss your investment strategy with one of our planners. Get in touch to book an appointment or call directly on 02 9328 0876.

This article was prepared by Dr Shane Oliver. Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist at AMP Capital is responsible for AMP Capital’s diversified investment funds. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.

General Disclaimer: This article contains information that is general in nature. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decisions based on this information. Please seek personal financial advice prior to acting on this information.