but it could have been much worse...

Key points

- 2019-20 saw a rough ride for investors as coronavirus hit resulting in small losses for well diversified investors.

- Key lessons for investors from the last financial year were to: maintain a well-diversified portfolio; timing market moves is hard; beware the crowd; turn down the noise; and don’t fight the Fed.

- With coronavirus risks still high, investment markets may see more short-term volatility. But over the next 12 months returns from a well-diversified portfolio are likely to be constrained, but okay.

Introduction

The past financial year was poor for investors as coronavirus knocked economies into what is likely to be their biggest hit since the 1930s. Shares were hit hard, but the blow was softened by a strong rebound in the June quarter. This note reviews the last financial year and takes a look at the outlook.

Pre and post covid

The past financial year can effectively be divided into two halves. The period from July last year into early this year saw generally strong returns from shares and growth assets, as fear of recession faded helped by central bank easing and a truce in the US/China trade war and gave way to expectations of some improvement in global economic growth. Despite devastating bushfires and a subdued growth outlook even the Australian share market made it to a record high in February. Against this backdrop, returns from government bonds were subdued.

This now seems like it was a different world as it all started to fade and ultimately reverse as the coronavirus epidemic started to become a problem in China in January. Initially it was hoped it would be contained to China (which successfully controlled it allowing a reopening of its economy from March) but from late February the number of cases escalated in Europe then the US, Australia and ultimately emerging countries, resulting in severe lockdowns driving sharp economic contractions in economic activity. So, between 20th February and 23rd March share markets collapsed by around 35% dragging down commodity prices. This also saw the $US surge and the Australian dollar plunge to around $US0.55.

However, from late March shares staged a rebound driven by policy stimulus, a decline in new covid cases, economic reopening and a rebound in economic data. From their March lows to June highs global shares rose 40% & Australian shares rose 35% and commodity prices and the $A also rebounded.

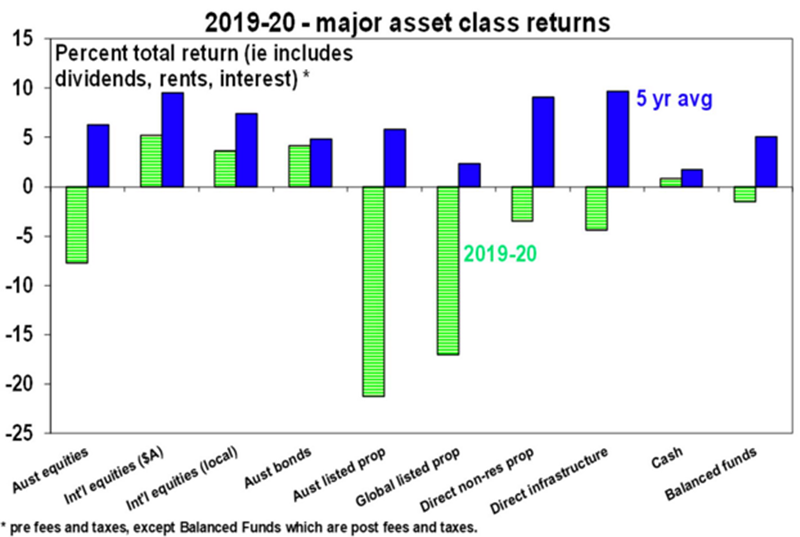

So, despite this wild ride, for the financial year as a whole global shares returned 5.2% in Australian dollar terms. This was led by the US share market which outperformed due to a heavy tech and health care exposure, a relatively low exposure to cyclical shares and massive Fed quantitative easing. Australian shares didn’t fare so well & still lost 7.7% for the financial year.

Cash and bank deposits had very low returns as the RBA cut the cash rate to 0.25% in March. But bonds had reasonable returns as plunging yields provided capital growth for investors. Despite the plunge in interest rates and bond yields, listed property saw double digit losses as the coronavirus driven slump in economic activity pushed up vacancies and depressed rents in retail and office properties. Returns on airports were similarly depressed weighing on direct infrastructure returns.

This all saw small negative returns for balanced growth superannuation funds of around -1.5% after fees and taxes. Of course, it would have been much worse were it not for the June quarter rebound in shares. The hit to super returns also followed several years of strong returns and the five-year average is just over 5% which is not so bad given (pre tax) bank deposit rates averaged around 2% and inflation averaged 1.5%.

Source: Thomson Reuters, AMP Capital

Like shares, Australian residential property had a roller coaster ride – first rising 10% on rate cuts and the Federal election before starting to slow as coronavirus hit.

Key lessons for investors from the last financial year

These include:

- Maintain a well-diversified portfolio – while shares and listed property had a rough ride, bonds and exposure to global shares and foreign currency provided some stability.

- Timing markets is hard – while it always looks easy in hindsight, getting out in February at the top and then getting back in March at the low would have been very hard to time.

- Beware the crowd at extremes – as is often the case shares hit bottom in March at a time of extreme investor pessimism.

- Turn down the noise – the noise around coronavirus is at fever pitch making it very hard to maintain focus on long term investing, so the best thing is to turn it down a notch.

- Don’t fight the Fed – despite near zero interest rates and high public debt levels, policy stimulus can still be applied on a massive scale and still impacts investment markets.

The negatives

There are a bunch of threats which are likely to lead to a further correction in shares in the short term, ongoing bouts of volatility and constrained returns. Here are the big ones.

- First, while some countries have got new coronavirus cases well down, it’s still on the rise globally particularly in emerging countries and the US and Victoria have seen a resurgence in cases. This is threatening a return to economically debilitating country wide lockdowns (as opposed to targeted measures). Even partial lockdowns will slow the recovery – eg, our rough estimate is that the new six-week lockdown of Melbourne, which accounts for about 20% of Australian GDP will knock nearly 1% off Australian GDP this quarter, which will slow the recovery (but not derail it as it should be offset by growth in other states).

- Second, the shutdowns will leave lasting collateral damage in terms of bankruptcies and higher unemployment as the embrace of technology has been sped up, companies cut costs and skills atrophy, all of which will weigh on growth.

- Third, in Australia the main collateral risk is that the combination of high unemployment, a collapse in underlying housing demand on the back of a plunge in immigration and a depressed rental market drive a sharp collapse in home prices triggering negative wealth effects.

- Fourth, the run up to the US election has the potential to drive increased share market volatility if it looks increasingly likely that Biden will win and raise taxes, and the risk is probably greater if President Trump decides he has nothing to lose and ramps up tensions with China and maybe Europe. With betting markets favouring a clean sweep by the Democrats some of the former is probably already priced, but an intensification of trade wars is probably not.

- Finally, shares are expensive on traditional metrics like PEs.

The positives

However, there are a bunch of positives providing an offset.

- First, several Asian countries have shown its possible to control the virus – notably China, South Korea, Taiwan and Japan. Maybe the SARS experience helps along with the culture of wearing masks. Surely, we can learn from them.

- Second, progress is continuing to be made in terms of vaccines and treatments for coronavirus. I am a bit sceptical about a vaccine, but the latter may be contributing to lower death rates. If deaths remain low compared to the first wave there is less risk of a return to hard lockdowns (Victoria excepted!) and less self-isolation.

- Third, policy makers remain committed to do whatever they can to support businesses, incomes and jobs with record levels of fiscal stimulus relative to GDP and massive monetary stimulus. This is different to normal recessions where it takes longer for policy makers to swing into action. To this end policy stimulus will be extended in the US and in Australia (with the Treasurer talking about another phase of income support and possibly bringing forward tax cuts).

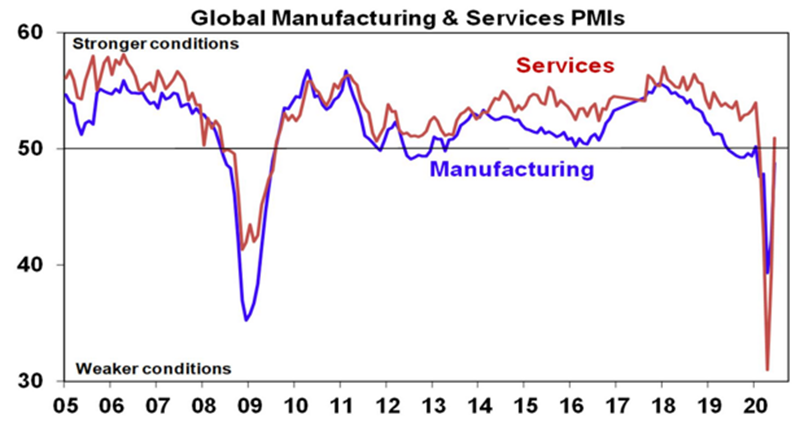

- Fourth, a range of economic indicators have seen a Deep V rebound from shutdown lows starting in China and then in developed countries, suggesting significant pent up demand. This is most evident in business conditions PMIs but also in retail sales. On balance we see a gradual bumpy economic recovery from here. Australian GDP is expected to contract -4.5% this year and grow 4% next year.

Source: Bloomberg, AMP Capital

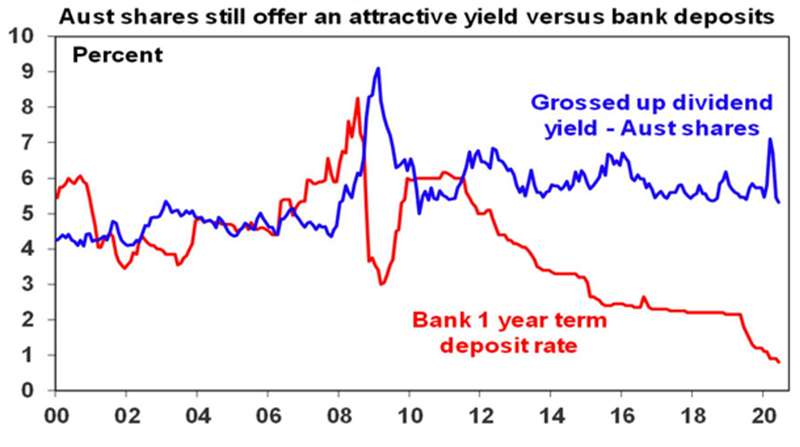

Source: RBA; AMP Capital

- Finally, the plunge in interest rates and bond yields have increased the present value of shares and other growth assets, which explains why price to earnings multiples are so high. Or looked at another way, shares remain attractive despite lower earnings and dividends because the alternatives like bank deposit rates are even less attractive.

What about the return outlook?

With coronavirus risks still high, investment markets may see more volatility. But over the next 12 months returns from a well-diversified portfolio are likely to be constrained but okay.

- After a strong rally from March lows shares remain vulnerable to short term setbacks given uncertainties around coronavirus and US/China tensions. But on a 6 to 12-month view shares are expected to see reasonable returns helped by a pick-up in economic activity & massive policy stimulus.

- Cash and bank deposit returns are likely to be poor at less than 1% as the RBA is expected to keep the cash rate at 0.25%. Investors still need to think about what they really want: if it’s capital stability then stick with cash, but if it’s a decent income flow then consider the alternatives.

- Low starting point yields are likely to result in low returns from bonds once the dust settles from coronavirus.

- Unlisted commercial property and infrastructure are ultimately likely to benefit from a resumption of the search for yield, but the hit to economic activity and hence rents from the virus will weigh heavily on near term returns.

- Home prices are expected to fall by around 5 to 10% into next year as higher unemployment, a stop to immigration and the weak rental market impact.

- Although the $A is vulnerable to bouts of uncertainty about the global recovery and US/China tensions, a continuing rising trend is likely if the threat from coronavirus recedes.

Loans and guarantees are helpful but they leave businesses more indebted, whereas actual fiscal stimulus provides a direct boost. So actual fiscal support is a better measure and on this front Australia at 10.6% of GDP has provided by far the strongest fiscal stimulus of G20 countries. What’s more, Australia’s centrepiece JobKeeper wage subsidy is superior to approaches taken by many other countries as it keeps people “employed”, minimises confidence zapping negative headlines around unemployment, preserves the employer/employee relationship, keeps workers getting paid and provides a subsidy to struggling businesses. Unemployment is likely to rise to around 10% which is bad, but its far better than the 15% that would likely occur in the absence of JobKeeper or 20% or so unemployment in the US.

Things to keep an eye on

The key things to keep an eye on are: coronavirus hospitalisations and deaths, as a guide to the degree of isolation; global business conditions PMIs and unemployment; US election prospects; and Australian house prices.

Does your investment strategy need a review?

Arrange a meeting to speak with one of our Financial Planners, either book a virtual meeting or call us to arrange an appointment on 02 4229 8533.

Article by AMP Capital

This article was prepared by Dr Shane Oliver. Dr Shane Oliver who provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.

General Disclaimer: This article contains information that is general in nature. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decisions based on this information. Please seek personal financial advice prior to acting on this information.